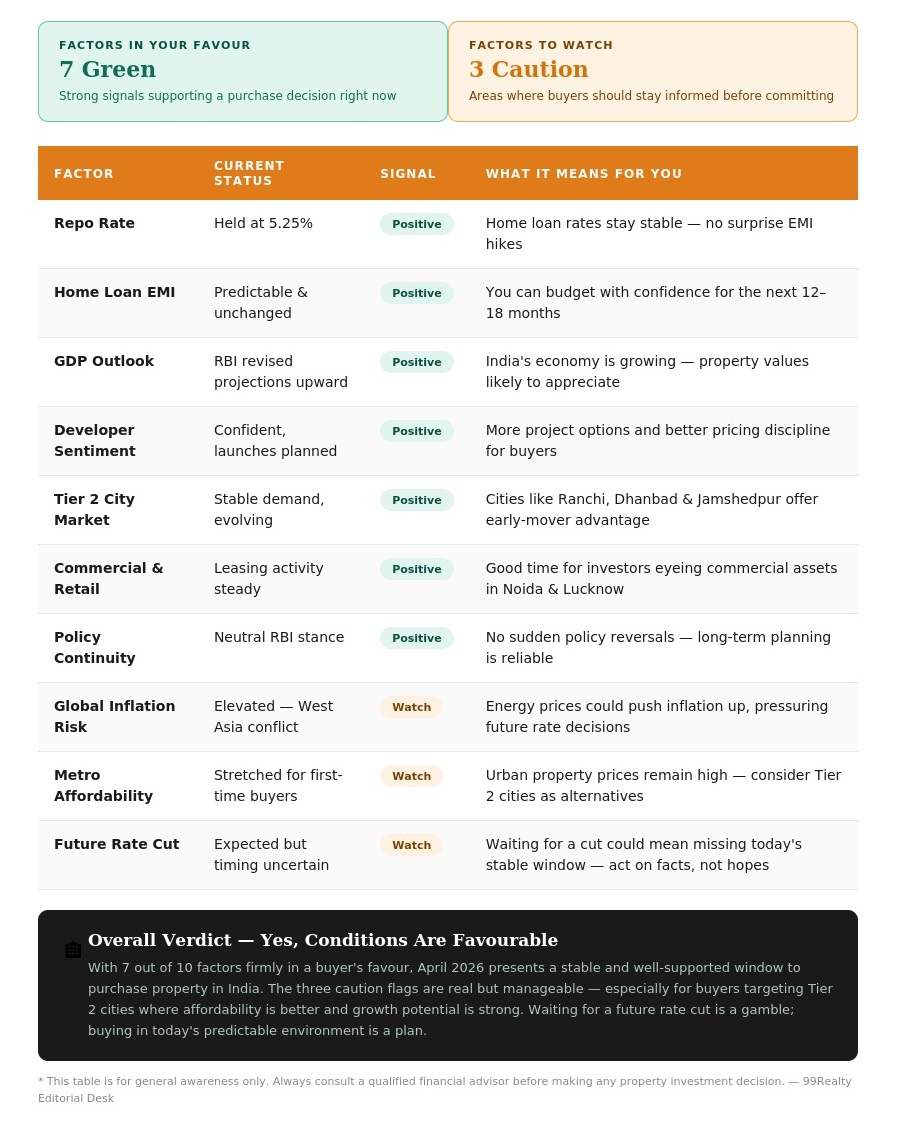

In boardrooms and on construction sites alike, few policy decisions carry as much weight for the Indian real estate sector as the Reserve Bank of India’s repo rate call. On April 8, 2026, the Monetary Policy Committee chose to keep the rate unchanged at 5.25% — a move that, on the surface, sounds like the absence of news. But for home buyers, developers, and investors watching closely, it is anything but.

The world outside India’s borders is anything but calm. Escalating conflict in West Asia has sent energy prices climbing, reviving the ghost of imported inflation. Global central banks are walking a tightrope between growth and price stability. Against this backdrop, the RBI’s “wait and watch” posture is less about indecision and more about strategic patience — the art of knowing when not to move.

“Stability in policy matters more than aggressive interventions. For homebuyers, it means EMIs remain predictable, making it easier to plan purchases with confidence.”— Nitin Shrivastava, Managing Partner, Big FM Realty

Why This Matters More Than a Rate Cut Would Have

Here’s the counterintuitive truth: sometimes a hold delivers more than a cut. A rate reduction signals concern — it tells markets that the economy needs a boost. A hold, paired with an upward revision in near-term GDP projections, signals something more valuable: quiet confidence. The RBI is essentially saying, “India’s fundamentals are sound, and we’re watching before we act.”

For real estate — a sector built on long-term planning and multi-year capital commitments — this kind of visibility is gold. Developers can price launches with greater precision. Banks won’t suddenly reprice home loan products. And buyers, most critically, can make purchase decisions without second-guessing what their EMI will look like six months from now.

What does a stable repo rate mean for your home loan? If the repo rate stays at 5.25%, home loan rates for most borrowers remain in a predictable band. A ₹50 lakh loan at a 25-year tenure sees no surprise jump in monthly outgo — giving first-time buyers the confidence to commit rather than wait.

The Affordable Housing Challenge Remains Real

It would be dishonest to paint this as a universally perfect outcome. Amit Modi of County Group put it plainly: a marginal rate cut would have offered “meaningful relief to homebuyers, especially first-time borrowers managing stretched affordability in key urban markets.” He’s right. In a city like Noida or Lucknow, where mid-income buyers are navigating rising property values against stagnant wage growth, even a 25-basis-point cut could have unlocked a new segment of demand.

Similarly, Sanjay Sharma of SKA Group noted that the affordable and mid-housing categories specifically could have benefited from further demand momentum. The tension between macro-caution and micro-relief is real — and it’s a conversation the Indian real estate sector will keep having as long as inflation risks persist.

Why Integrated Living Is Redefining Luxury Housing in India

The Tier 2 City Story Gets More Interesting

Perhaps the most overlooked dimension of this decision is its impact on emerging markets. Udit Jain of One Group pointed out that in Tier 2 cities — markets still finding their footing — buyers “tend to be more cautious and value clarity over short-term incentives.” Stable home loan rates build exactly that clarity. For cities like Dhanbad, Ranchi, and Jamshedpur, where real estate cycles are less mature but appetite is growing, a predictable interest rate environment could prove to be a quiet accelerant.

Commercial Real Estate Gets Visibility Too

The residential market often hogs the spotlight, but the commercial segment has its own story here. Sanchit Bhutani of Group 108 noted that a steady repo rate “provides greater visibility on borrowing costs, fostering confidence among developers, investors, and occupiers alike.” Retail real estate specifically benefits — as Ajendra Singh of Spectrum Metro pointed out, brands expanding their footprint need predictable financing. Stable rates mean more structured leasing activity and healthier occupancy across organised retail spaces.

The 99Realty Takeaway: This is a Buyer’s Signal, Not a Bystander’s Moment

If you have been sitting on the fence about a property purchase — whether in Tier 1, 2 or beyond — the RBI’s decision is a quiet green light. Not because everything is perfect, but because the conditions you see today are the conditions you can plan around. EMIs are predictable. Lending sentiment is positive. And in a world of geopolitical uncertainty, India’s real estate sector continues to hold its ground as a stable, long-term asset class.

The window of rate stability is real. Whether it lasts another quarter or extends further depends on how global tensions evolve. But right now, in April 2026, the message from Mint Street to Main Street is clear: the ground is firm. Take your next step.

Disclaimer : The information published in this article is intended for general awareness and educational purposes only. 99Realty does not provide financial, legal, or investment advice. The views and opinions quoted from industry experts are their own and do not represent the official position of 99Realty. Readers are advised to consult a qualified financial advisor before making any investment decisions. While we strive to ensure the accuracy of information at the time of publishing, 99Realty is not liable for any decisions made based on the content of this article.

Need Help?

Need help evaluating a property or planning your next move in the market?

Reach out to 99 REALTY – your trusted real estate partner for smarter choices.

Subscribe to get updates on our latest posts and market trends.

Join The Discussion