A home loan is a financial product offered by banks and financial institutions to assist individuals in purchasing residential properties. The borrower agrees to repay the loan amount, along with interest, over a specified tenure through Equated Monthly Installments (EMIs). A well-planned down payment is pivotal in securing favorable home loan terms in India. It not only reduces your loan burden but also enhances your credit worthiness, leading to better interest rates and manageable EMI.

📊 RBI Guidelines on Down Payment and Home Loan

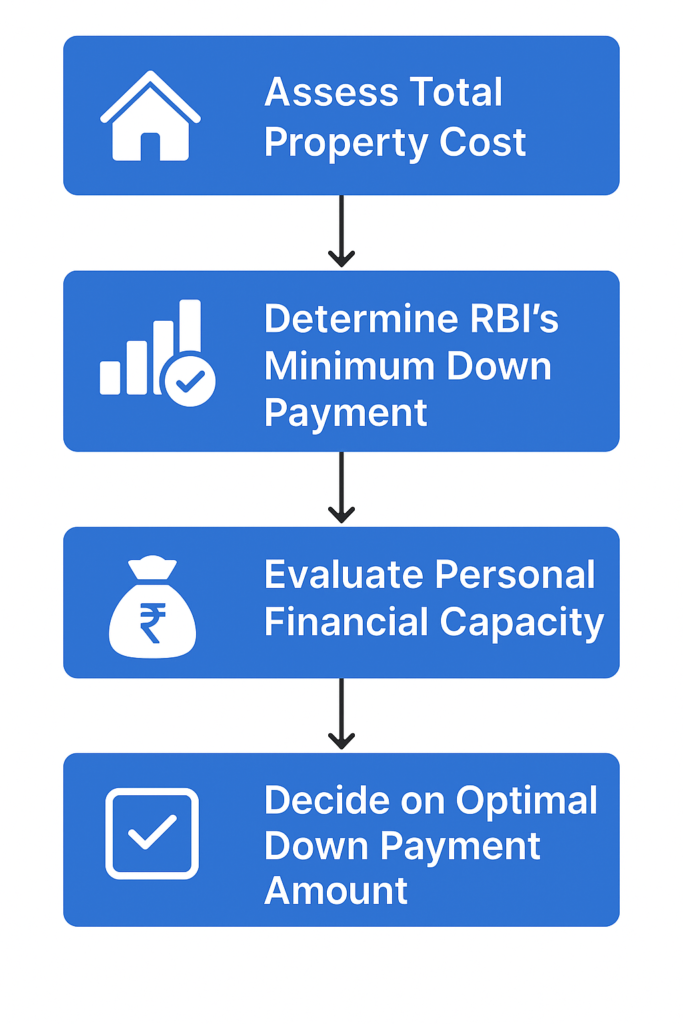

The LTV ratio determines the maximum loan amount a borrower can avail against the property’s value. As per RBI’s guidelines:

RBI Guidelines: Home Loan LTV Ratio

| Property Value | Maximum LTV | Minimum Down Payment |

|---|---|---|

| Up to ₹30 lakh | 90% | 10% |

| ₹30 lakh to ₹75 lakh | 80% | 20% |

| Above ₹75 lakh | 75% | 25% |

Note: Stamp duty, registration, and documentation charges are excluded from LTV calculation.

Interest Rate Benchmarking

RBI mandates that home loan interest rates be linked to external benchmarks, such as the repo rate. This ensures that changes in the central bank’s policy rates are transparently and promptly reflected in lending rates.

Prepayment Charges

Borrowers opting for floating-rate home loans can prepay their loans without incurring any prepayment penalties. This flexibility encourages borrowers to reduce their debt burden when possible.

Documentation and Transparency

Lenders are required to provide clear and comprehensive information regarding loan terms, interest rates, fees, and charges. This ensures that borrowers make informed decisions and understand their obligations fully.

Moratorium and Restructuring Provisions

In situations of financial hardship, such as job loss or medical emergencies, borrowers can request a moratorium or restructuring of their home loans. RBI has provided guidelines to facilitate such relief measures, ensuring borrowers are not unduly burdened during challenging times.

📝 Factors Influencing Home Loan Eligibility

- Credit Score: A higher credit score indicates better creditworthiness, increasing the chances of loan approval.

- Income Stability: Consistent and verifiable income assures lenders of the borrower’s repayment capacity.

- Existing Liabilities: A lower debt-to-income ratio is favorable, as it suggests manageable existing financial obligations.

- Age and Employment Type: Younger borrowers with stable employment (salaried or self-employed) are often preferred.

💡 Benefits of a Higher Down Payment

- Reduced Loan Amount: Lower principal leads to decreased interest over the loan tenure.

- Improved Loan Eligibility: Higher upfront payment enhances your debt-to-income ratio.

- Negotiation Leverage: Demonstrates financial stability, potentially securing better interest rates.

- Protection Against Market Fluctuations: Minimizes the impact of property value changes.

Also Read: Decoding Interest Rates How They Impact Your Home Loan and Mortgage Payments

🧮 Calculating Your Ideal Down Payment

Determining the right down payment involves assessing your financial health and future commitments.

💰 Strategies to Accumulate Down Payment

- Personal Savings: Utilize fixed deposits, recurring deposits, and savings accounts.

- Liquidate Investments: Consider redeeming mutual funds or selling socks.

- EPF/PPF Withdrawals: Permissible under specific conditions for housing purposes.

- Gold Asses: Pledge or sell gold to raise funds.

- Government Schemes: Leverage benefits from programs like PMAY for eligible individuals.

⚠️ Common Pitfalls to Avoid

- Overextending Finances: Avoid exhausting all savings, leaving no emergency buffer.

- Ignoring Additional Costs: Account for registration, stamp duty, and furnishing expenses.

- High-Interest Borrowing: Refrain from using personal loans or credit cards for down payments.

- Neglecting Credit Score: A low score can affect loan approval and terms.

A strategic approach to your home loan down payment can significantly impact your financial well-being. By understanding RBI guidelines, leveraging available resources, and avoiding common mistakes, you can ensure a smoother path to homeownership.

RBI’s Consecutive Repo Rate Cut to 6% Triggers Real Estate Revival Across India

📚 FAQs

Q1: What is the minimum down payment required for a home loan in Indi?

A: It ranges from 10% to 25% of the property’s value, based on RBI’s LTV guidelines.

Q2: Can I get a home loan without a down payment?

A: No, RBI mandates a minimum borrower contribution; zero down payment loans are not permitted.

Q3: Does a higher down payment reduce my home loan interest rat?

A: Yes, it can lead to better interest rates due to reduced lender risk.

Q4: Are there government schemes to assist with down payment?

A: Yes, schemes like PMAY offer subsidies that can ease the financial burden.

Q5: Can I use EPF or PPF funds for the down payment?

A: Yes, under certain conditions, withdrawals are allowed for housing purposes.

Subscribe to get updates on our latest posts and market trends.

Join The Discussion