In the intricate world of home financing, selecting the right interest rate structure is not just a financial decision — it’s a strategic move that can significantly impact your long-term affordability, budgeting discipline, and investment returns. At 99Realty Blogs, we understand how crucial this choice is. This in-depth guide explores fixed vs floating interest rates in India, dissecting every element that matters to homebuyers and investors alike.

Ultimate Guide to Home Loan Down Payments in India (2025)

What is a Fixed Interest Rate?

A fixed interest rate locks your home loan EMI at a constant rate throughout the tenure. Regardless of fluctuations in the market, your repayment amount remains unchanged.

Key Characteristics:

- EMI remains the same.

- Insulated from RBI policy changes or inflationary pressures.

- Offered slightly higher than prevailing floating rates to hedge against market risks.

Advantages:

- Budgeting Clarity: You know exactly what to pay each month.

- Inflation Shield: No impact from rising repo rates or market volatility.

- Ideal for Stable Income Profiles: Salaried individuals, retirees, or anyone preferring predictable outflows.

Disadvantages:

- No Benefit During Rate Cuts: Market dips won’t reduce your EMI.

- Higher Initial Rates: Fixed rates are generally 0.5%–1.5% higher than floating rates.

- Foreclosure Charges: Lenders may levy higher prepayment penalties.

What is a Floating Interest Rate?

A floating interest rate varies based on prevailing market conditions. It’s tied to external benchmarks like the RBI Repo Rate or internal ones like MCLR (Marginal Cost of Funds Based Lending Rate).

Key Characteristics:

- EMI may increase or decrease.

- Tracks market trends and RBI’s monetary policy.

- Often starts lower than fixed interest rates.

Advantages:

- Lower Initial Costs: Entry EMIs are budget-friendly.

- Savings Potential: Interest rates fall, you save.

- Flexible Prepayment: Usually no or low foreclosure penalties.

Disadvantages:

- EMI Uncertainty: Monthly payments fluctuate.

- Difficult Budgeting: Requires financial agility and buffer planning.

- Rate Hike Exposure: Rising interest environment can derail cash flow plans.

RBI’s Consecutive Repo Rate Cut to 6% Triggers Real Estate Revival Across India

Fixed vs Floating Interest Rates: Detailed Comparison Table

| Parameter | Fixed Interest Rate | Floating Interest Rate |

|---|---|---|

| EMI Stability | Constant throughout the tenure | Varies based on market changes |

| Market Dependency | Immune to market rate fluctuations | Highly responsive to RBI rate and inflation changes |

| Best For | Risk-averse, fixed income individuals | Financially flexible, market-savvy borrowers |

| Initial Interest Rate | Slightly higher than floating | Typically lower than fixed |

| Prepayment Charges | Often high, especially in early years | Usually low or NIL |

| Long-Term Cost Efficiency | Higher if market rates stay low | Lower if interest rates decline during tenure |

| Tenure Suitability | Short to medium term | Medium to long term |

| Risk Exposure | Low | Moderate to High |

When to Choose Fixed Interest Rate?

You should consider a fixed interest rate if:

- You are risk-averse and prioritize financial predictability.

- The interest rate cycle is expected to rise, and locking now secures lower EMIs.

- Your monthly income is fixed, such as salary or pension-based inflows.

- You’re buying a property for self-use and don’t expect to prepay early.

When to Choose Floating Interest Rate?

Opt for a floating interest rate if:

- You expect interest rates to drop or stay neutral in the coming years.

- Your income is variable or scalable — such as freelancers, entrepreneurs, or commission-based earners.

- You plan to prepay the loan within a few years through bonuses, inheritance, or investments.

- You’re comfortable with risk and have surplus liquidity for EMI variations.

Which Interest Rate Is Better?

The decision isn’t binary — it’s contextual. Here’s a quick strategy to decide:

| Scenario | Recommended Interest Type |

|---|---|

| Interest rates expected to rise | Fixed |

| Long tenure (15+ years) planned | Floating |

| Steady monthly income | Fixed |

| Anticipated salary hikes or windfalls | Floating |

| Seeking EMI stability for family budgeting | Fixed |

| Planning partial prepayments regularly | Floating |

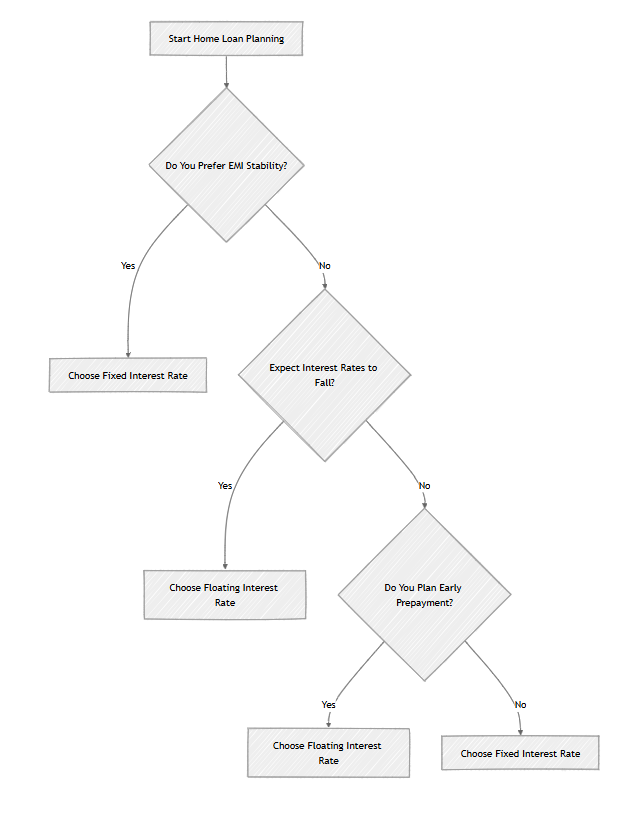

Recommended Visual: Interest Rate Decision Flowchart

Can You Switch Between Fixed and Floating Rates?

Yes. Most Indian banks allow switching between fixed and floating rates during the tenure. However, charges apply:

- Conversion Fee: Generally 0.5% to 1% of the outstanding loan.

- Documentation: Revised sanction letter and rate structure required.

- Approval: Subject to lender’s discretion and current market offerings.

If you’re planning to repay your home loan early or expect interest rates to fall, a floating rate could save you more in the long run.

Expert Insights: How RBI Rate Changes Influence Floating Rates

The RBI Repo Rate directly influences floating-rate loans. When the RBI cuts the repo rate, banks often reduce lending rates, lowering your EMI.

- Repo Rate Down → Lower EMIs

- Repo Rate Up → Higher EMIs

For example, a 50 basis points cut on a ₹50 lakh loan at 8.5% interest over 20 years can reduce your EMI by approx. ₹1,600/month.

Real-World Case Study: Fixed vs Floating Over 10 Years

Let’s assume a ₹50 lakh loan for 10 years.

| Metric | Fixed @ 9% | Floating @ 8% avg |

|---|---|---|

| EMI | ₹63,345 | ₹60,662 |

| Total Interest Paid | ₹26.01 lakhs | ₹23.79 lakhs |

| Potential Savings | ❌ | ✅ ₹2.22 lakhs approx. |

Insight: Even a 1% lower average rate can save you ₹2–3 lakhs in interest over a decade.

Conclusion

Selecting between fixed and floating interest rates for home loans in India requires clear foresight and understanding of your financial landscape. Fixed rates guarantee peace of mind and budgeting simplicity, while floating rates reward those who can navigate economic cycles and absorb short-term volatility.

Make your decision by aligning:

- Your income type

- Loan tenure

- Interest rate forecasts

- Flexibility in EMI handling

Only then will your home loan not just be a liability — but a smart financial tool.

FAQs: Fixed vs Floating Home Loan Rates

Q1. Is fixed interest rate always higher than floating?

Yes, typically fixed rates are higher to hedge future risks.

Q2. Can I change the type of interest rate mid-loan?

Yes, banks allow conversions but charge a conversion fee.

Q3. Which is better for long-term home loans?

Floating rates usually offer better savings over 15+ years.

Q4. Do floating interest rates change monthly?

No, changes are periodic—often quarterly or biannually, based on benchmark revision frequency.

Q5. What are MCLR and repo rate in this context?

MCLR is the internal lending rate of a bank; repo rate is set by RBI and serves as the external benchmark for floating loans.

Need Help?

Need help evaluating a property or planning your next move in the market?

Reach out to 99 REALTY – your trusted real estate partner for smarter choices.

Subscribe to get updates on our latest posts and market trends.

Join The Discussion